Non-recoverable depreciation appears in your insurance claim when the insurance company evaluates how much your property is worth today. This affects you because it reduces what you receive after a claim. In most cases, this reduction is not immediately obvious and many policyholders don’t realize how much value they are losing from their claim.

If you want to understand what non-recoverable depreciation is, you need to look at how insurers evaluate the value over time of your property. Every item, whether it’s a roof, flooring, or structural component, loses value over time due to age, usage, and wear. This reduction is known as depreciation, and it is factored into how your insurance claim is calculated.

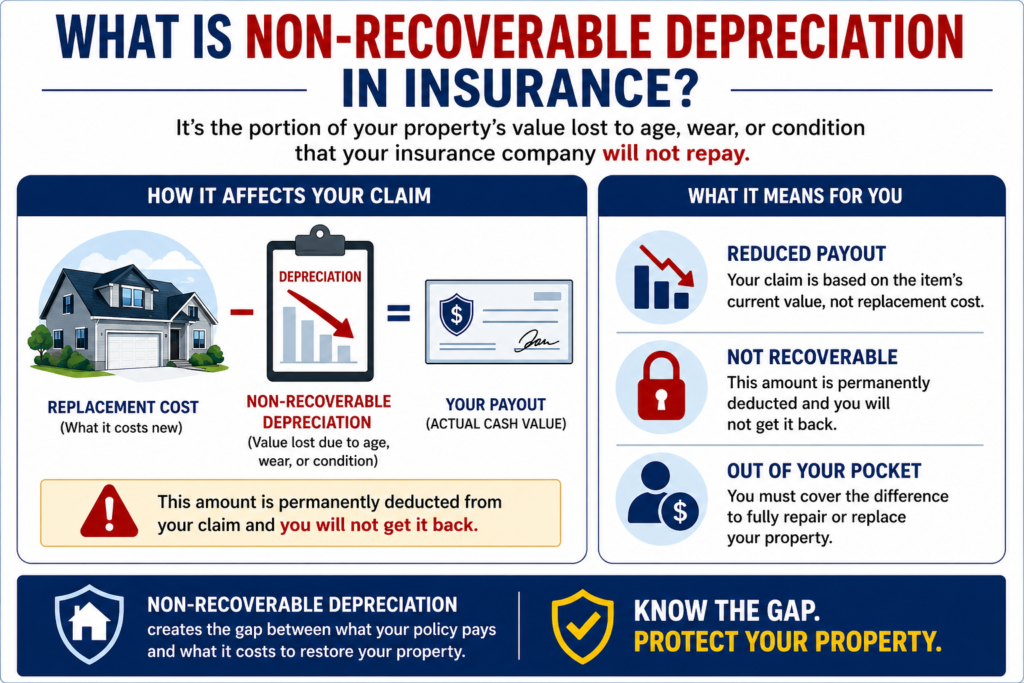

The insurer starts with the replacement cost, then subtracts depreciation to determine the actual cash value. The reason this happens is that the insurer is not paying for a brand-new item by default but for the item’s condition at the time of loss.

When that deducted amount is labeled as non-recoverable depreciation, it means it is permanently removed from your settlement. You will not recover it, even if you replace or repair the damaged property. That deducted portion becomes your responsibility to cover.This is where many claims shift from expectation to reality. Policyholders expect full replacement, but the insurance company will often limit payment to actual cash value, leaving a gap that you must cover, and in many cases, that gap can be substantial.

What Does Non-Recoverable Depreciation Mean for Homeowners

For homeowners, non-recoverable depreciation determines how much of the cost to replace your property comes out of your own pocket.

When your home insurance policy is based on actual cash value, the insurer evaluates what your damaged property is worth today, not what it costs to replace it. The logic behind this is that the insurance company assumes the item has already lost part of its usable life and it’s not going to cover its full cost but its depreciated cost.

That difference between current value and replacement cost is where non-recoverable depreciation applies. This is often shown on your estimate as less non-recoverable depreciation. That line is money that has been deducted and will not be paid by the insurance, even if you complete repairs or replacements.

The result is predictable. Many insurance claims are settled below the actual costs required to restore the property and the amount of the depreciation is covered by the homeowner. This does not necessarily mean the claim is denied. It means the claim is reduced. This is where policyholders unknowingly absorb thousands in losses, often because the reduction is presented as a standard calculation rather than a negotiable outcome.

Non-Recoverable Depreciation Vs. Recoverable Depreciation Explained

To fully assess your coverage, you must understand the difference between recoverable depreciation and non-recoverable depreciation, because this determines whether you can ever reach full replacement cost.

- Recoverable depreciation is withheld temporarily. If your policy includes replacement cost coverage, you can claim it back after completing repairs. The reason insurers do this is to make sure the work is completed before issuing the remaining payment. The reasoning is that the money they pay should go toward repairing the home, and not to pay for something else.

This means you may eventually receive the full replacement cost value, but only after meeting those conditions.

- In contrast, non-recoverable depreciation is never reimbursed. It is deducted upfront and remains excluded from your payout regardless of what actions you take. The insurer considers this portion permanently lost due to age or condition.

This difference between recoverable and non-recoverable is not always clear, but it defines the outcome of your insurance claim. In many cases, policyholders assume all depreciation works the same way. In reality, whether depreciation is recoverable depends entirely on the type of policy.

What Is Less Non-Recoverable Depreciation on an Insurance Estimate

When you receive the estimate from your insurance company, the phrase “less non-recoverable depreciation” is one of the figures that pops up and it’s what you are losing from the claim.

So, what is less non-recoverable depreciation? It is the amount subtracted from the replacement cost value to calculate your final payout. It is based on value over time, and reflects the condition of the item right before the damage occurred. The accuracy of that adjustment depends entirely on how the insurer assesses the condition in the first place after your insurance claim.

For example:

1. Replacement cost: $20,000

2. Total depreciation: $8,000

3. Less non-recoverable depreciation: $8,000

4. Final payout (actual cash value): $12,000

That $8,000 is your financial responsibility if you want to complete a full replacement cost repair.

What Does Less Non-Recoverable Depreciation Mean on Your Claim

If you are asking “what less non-recoverable depreciation means”, it usually means your insurance company has structured your claim in a way that limits your payout based on their interpretation of the item’s condition. It means:

- Your settlement is based on actual cash value

- A portion of the value has been permanently deducted

- You will not receive the full amount needed for restoration

This reduction is based on assumptions about age, usage, and condition. If those assumptions are incorrect, the reduction is also incorrect.This is one of the most common reasons insurance claims are underpaid without being formally denied. The claim is approved, but the valuation is reduced.

Why Insurance Companies Apply Non-Recoverable Depreciation

When insurance companies apply non-recoverable depreciation, they are managing financial exposure across a large volume of claims.

In high-risk markets like Florida, insurers face frequent property damage events. To remain profitable, they must control total payouts. One of the main ways to save money is through how depreciation is calculated.

This leads to a consistent pattern:

- Damage is evaluated conservatively.

- Depreciation is applied based on generalized assumptions.

- Settlements match actual cash value instead of full replacement cost.

The same damage can be interpreted differently depending on how it is categorized. This interpretation directly affects the payout.

This is why two evaluations of the same property can produce different results, and why many policyholders receive less than expected without realizing the evaluation itself can be questioned.

How Non-Recoverable Depreciation Affects Your Insurance Payout

The impact of non–recoverable depreciation is significant because instead of paying the full replacement cost, the insurance company pays the actual cash value, which reflects the reduced value over time of the item. This is where the financial impact turns real, and the larger the damage, the larger the gap.

Non-Recoverable Depreciation on Roof Claims: What You Need to Know

A roof is one of the most heavily depreciated components in any insurance claim, and therefore one of the largest sources of financial loss. Because a roof naturally deteriorates, insurers apply significant depreciation and reduce the value assigned to the damaged property. The reasoning is based on lifespan, but the accuracy depends on how that lifespan is estimated.

If the condition of the roof was better than assumed, or if maintenance extended its usability, the applied non-recoverable depreciation may be overstated. In many cases, the difference between replacement cost and actual cash value for a roof determines whether repairs are financially possible without additional out-of-pocket expenses.

How to Check If Non-Recoverable Depreciation Was Calculated Correctly

To determine whether your insurance company applied non-recoverable depreciation correctly, you need to review the assumptions behind the calculation. This includes:

- The assigned age of the item

- Its condition before the damage

- The lifespan used in the estimate

- Local cost to replace standards

If any of these factors are inaccurate, the actual cash value is also inaccurate. This matters because the entire reduction is based on these inputs. If the inputs are wrong, the deduction is inflated.

Can You Recover Non-Recoverable Depreciation or Reduce It

While non-recoverable depreciation is defined as non-reimbursable, the amount itself is not always fixed. In many cases, the issue is not whether depreciation exists, but whether it was calculated correctly. You may be able to:

- Challenge the condition assessment.

- Provide documentation showing better maintenance.

- Show updated estimates for the replacement cost value.

This does not eliminate depreciation, but it can reduce the amount that will be deducted, which directly increases your payout.

Common Mistakes Insurance Companies Make with Non-Recoverable Depreciation

The way insurance companies apply depreciation is not always precise because it often relies on generalized assumptions rather than item-specific evaluations. Common issues include:

- Overestimating age or wear.

- Using standard depreciation rates.

- Ignoring maintenance or upgrades.

- Misclassifying items as non-recoverable depreciation.

Each of these mistakes increases the amount deducted from your claim, which means the financial loss increases as well, at your expense.

How to Dispute Non-Recoverable Depreciation on Your Claim

The way to dispute non-recoverable depreciation is to challenge how your insurance claim is calculated from the beginning, for example, value over time. Insurance assumptions determine how much depreciation will be deducted and how much you receive.

To challenge it effectively, you must provide verifiable data that forces a recalculation of the claim. This includes:

- Independent inspections that establish the true condition of the property.

- Contractor estimates that reflect the real replacement cost and scope of repairs.

- Documentation aligned with your insurance policy that supports coverage and valuation.

When the underlying inputs change, the insurance claim must be recalculated. That recalculation often reduces the depreciation applied and increases the actual cash value payout.

How a Public Adjuster Helps with Non-Recoverable Depreciation

A public adjuster changes the outcome of a claim by changing who defines the numbers the insurance company relies on. In a standard insurance claim, the valuation is built internally. The insurer determines the scope of damage, the replacement cost, and how much depreciation will be deducted. Those three variables, scope, cost, and depreciation, are what control your final payout.

When a public adjuster is involved, those variables are no longer defined solely by the insurer. Instead of relying on internal estimates, the claim is rebuilt with independent inspections that often establish additional damage, more accurate cost-to-replace calculations, and item-specific evaluations of value over time. This directly affects how depreciation is calculated, and in many cases, reduces the amount classified as non-recoverable depreciation.

PICC Fla approaches the claim from this position. The property is evaluated in person, the full scope of loss is documented, and the numbers presented to the insurer are supported by real-world pricing and condition assessments. The insurance company is responding to a competing, evidence-based valuation that is harder to reduce without justification.

Because PICC FLA works on a contingency basis, usually 10% to 20%, compared to attorney fees that may reach 40%, their incentive is directly tied to increasing your settlement, not simply processing the claim. This is why many claims increase in value after an independent evaluation. The damage has not changed. The way it is measured and presented has.

When Non-Recoverable Depreciation Is Applied (ACV Vs. RCV Policies)

The way non-recoverable depreciation is applied depends on the type of insurance policy you have. If your policy is based on Actual Cash Value (ACV), the insurance company only pays what the item is worth today. That means depreciation is fully non-recoverable, and you will have to cover the difference yourself.

If your policy is based on Replacement Cost Value (RCV), the process works differently. The insurer may first pay you the reduced amount (after depreciation), but once you complete the repairs or replacements, you can claim back the remaining portion. This is called recoverable depreciation. In simple terms:

- ACV policy: You don’t get the full amount, and the gap is your responsibility

- RCV policy: You can eventually get the full amount, but only after you finish the work

This is why two people with similar damage can receive very different payouts if their insurance policies are structured differently.

Steps to Maximize Your Payout When Non-Recoverable Depreciation Is Applied

To maximize the financial outcome of your insurance claim, you must present and evaluate it properly, because most policyholders rely on the insurer’s initial evaluation, which is often the lowest defensible version of the claim. This involves:

- Documenting all property damage.

- Verifying how depreciation is calculated.

- Securing independent estimates.

- Reviewing your insurance policy.

Get Help with Non-Recoverable Depreciation Claims Today

If your insurance claim includes non-recoverable depreciation, there’s a good chance you’re being paid less than you should. Most settlements are based on the insurance company’s assumptions, not the true cost to restore your property.

At PICC Fla, a public adjusting firm, we re-evaluate your claim from the ground up, and inspect the damage in person, to correct the numbers, and push for the payout your policy actually allows. With no upfront fees, a no recovery, no fee model, and a free policy review, there’s nothing to lose, only what you may be leaving behind.