PICC Public Adjusters

author

Blog posts:82

Join date:

May 21, 2025

How to File a Home Insurance Claim in Florida

Property damage claims in Florida don’t remain simple for long. A roof leak after a storm may initially appear to be isolated to one room before water spreads through the insulation and adjacent walls. A plumbing failure beneath a sink may affect cabinetry and flooring systems before visible deterioration appears. Even relatively small losses, such as AC leaks or water heater failures, can evolve into full restoration projects if moisture becomes trapped beneath flooring materials or within wall cavities. For many homeowners, the challenge is how to file a home insurance claim. The greater difficulty often involves documenting the loss, preserving evidence, understanding policy limitations, and making sure the damage is identified to its full extent before any repair begins. In particular, this becomes important in Florida, where hurricanes, roof damage, plumbing failures, and water intrusion claims happen regularly, and certain forms of structural deterioration are not immediately visible during an initial inspection. Understanding how to file a homeowners’ insurance...

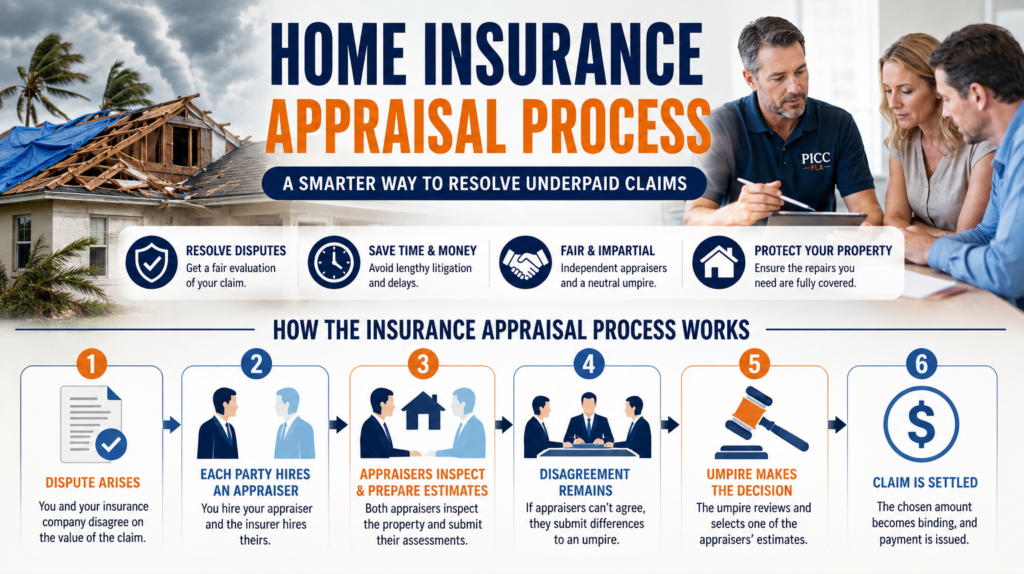

Home Insurance Appraisal Process

Insurance appraisal can be a valuable solution when you believe your property damage claim has been undervalued. Whether you are dealing with hurricane damage, water intrusion, fire loss, roof damage, or another covered event, understanding the appraisal process can help you make informed decisions about your claim. This guide explains how insurance appraisal works, when it may be appropriate, and how experienced professionals can help you pursue a fair settlement while avoiding unnecessary delays and costly litigation. At PICC FLA, we assist homeowners and business owners throughout the insurance appraisal process, providing free property inspections, complimentary policy reviews, and no recovery, no fee representation to help clients seek the compensation they may be entitled to receive. Call Us Today For A FREE Claim Analysis What Is a Home Insurance Appraisal? A home insurance appraisal is a dispute resolution procedure used when the insured and the insurance company disagree regarding the financial value of a covered insurance claim. These disputes commonly...

What to Do When Your Homeowners Insurance Claim Is Denied in Florida

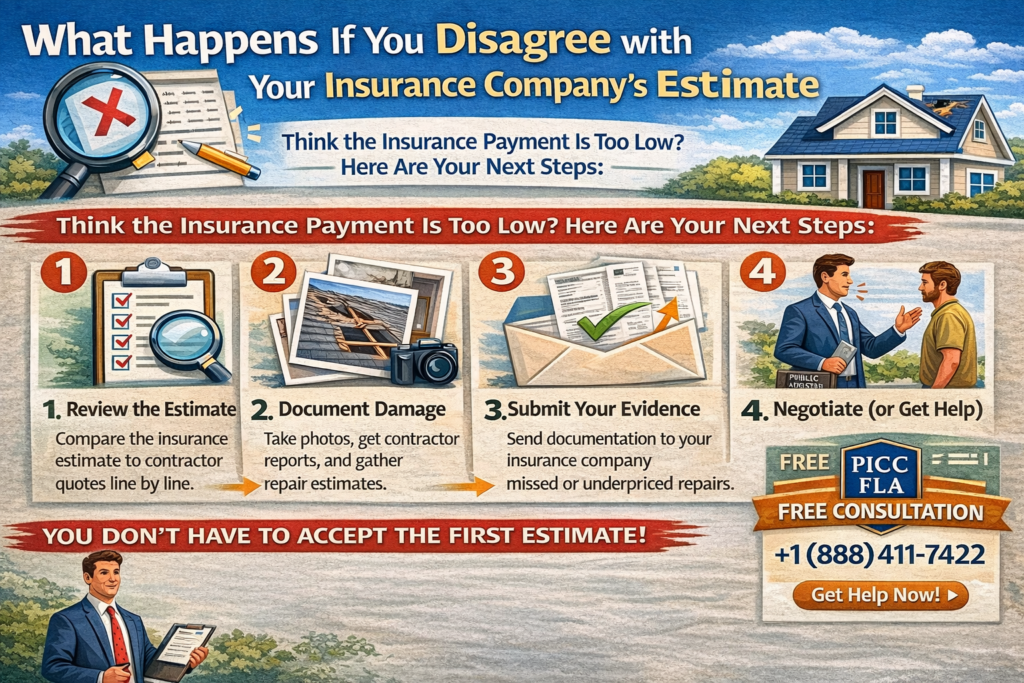

A homeowner’s insurance claim denied notice can be frustrating, especially when your property is already damaged, and repair costs are rising. Many Florida homeowners receive a denied home insurance claim after hurricanes, roof leaks, broken pipes, AC overflows, fire damage, or water intrusion, often because the insurance company disputes the cause of loss, limits the scope of repairs, or overlooks hidden damage during the inspection. The good news is that a denial does not always mean your claim is over. In many cases, homeowners discover that important damage was missed, repair costs were underestimated, or policy provisions were interpreted too narrowly. If you’re wondering what to do if homeowners’ insurance denies a claim or how to appeal a denied home insurance claim, understanding the true extent of the damage is often the first step toward a successful outcome. At PICC FLA, we work with homeowners facing denied property insurance claims every day. Our team performs detailed property inspections, reviews policy...

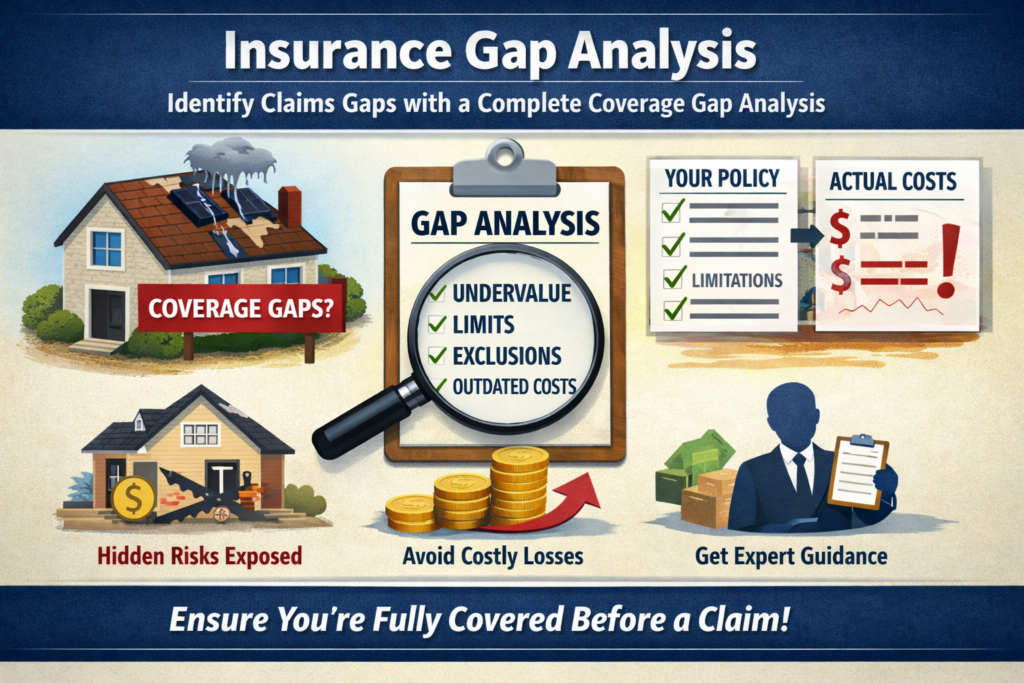

What Is Non-Recoverable Depreciation in Insurance

Non-recoverable depreciation appears in your insurance claim when the insurance company evaluates how much your property is worth today. This affects you because it reduces what you receive after a claim. In most cases, this reduction is not immediately obvious and many policyholders don’t realize how much value they are losing from their claim. If you want to understand what non-recoverable depreciation is, you need to look at how insurers evaluate the value over time of your property. Every item, whether it’s a roof, flooring, or structural component, loses value over time due to age, usage, and wear. This reduction is known as depreciation, and it is factored into how your insurance claim is calculated. The insurer starts with the replacement cost, then subtracts depreciation to determine the actual cash value. The reason this happens is that the insurer is not paying for a brand-new item by default but for the item’s condition at the time of loss. When that...

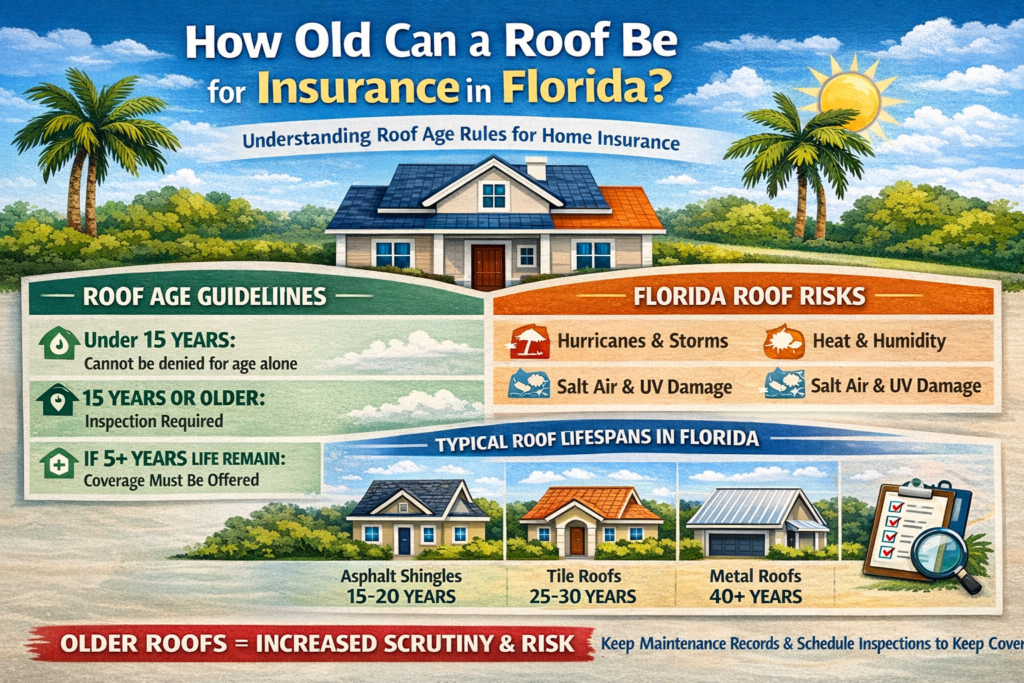

How Old Can a Roof Be for Insurance in Florida?

In Florida, a roof is more than just part of a home’s structure. For insurers, it is one of the strongest predictors of future claims. That connection explains why many Florida homeowners first encounter insurance problems at renewal, long before any visible damage appears. Letters requesting inspections, rate increases, or policy changes often arrive even when the roof still looks intact. The reason lies in how insurers evaluate risk, how Florida law limits those decisions, and how roofing age affects insurance coverage long before any failure occurs. In this article, we explain how these factors work together to help homeowners avoid sudden coverage issues and respond appropriately when insurers begin asking questions. Why Roof Age Drives Insurance Decisions in Florida Florida produces a unique insurance environment. Wind, humidity, salt air, and intense ultraviolet exposure accelerate the deterioration of roofing materials. Industry data consistently shows that roof-related losses are a large share of residential property claims across the state. Insurance companies...

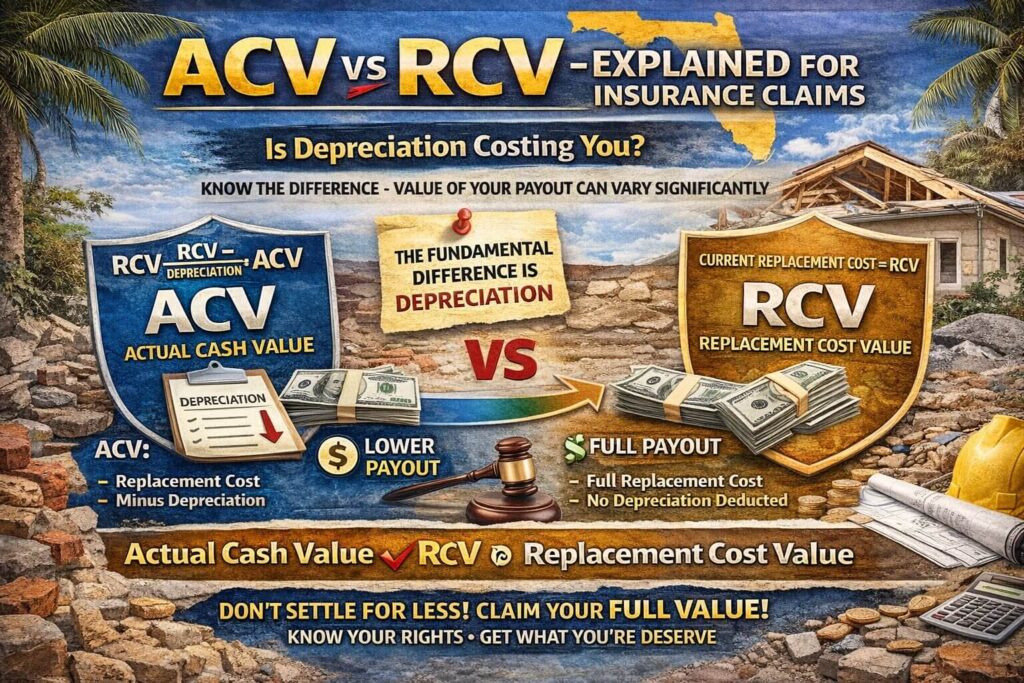

ACV vs RCV – Explained for Insurance Claims

The way an insurance claim gets calculated often matters more than the damage itself. Many homeowners expect their insurance policy to cover the full cost of fixing or replacing what was lost. However, the reality looks very different once terms like ACV and RCV appear on the estimate. This guide explains the real difference between ACV vs. RCV, how insurance companies use these methods, and what Florida property owners can do to protect the value of their insurance claim and understand the difference. What Is Replacement Cost Value in Insurance? Replacement cost refers to the amount of money that’s required to repair or replace damaged property with new materials of a similar kind and quality. In insurance, this method focuses on the current cost of replacing items today, not what they were worth years ago, and is commonly referred to as replacement cost insurance. When a policy provides replacement cost coverage, the goal is restoration. The damaged roof, flooring, cabinets,...