In Florida, a roof is more than just part of a home’s structure. For insurers, it is one of the strongest predictors of future claims. That connection explains why many Florida homeowners first encounter insurance problems at renewal, long before any visible damage appears.

Letters requesting inspections, rate increases, or policy changes often arrive even when the roof still looks intact. The reason lies in how insurers evaluate risk, how Florida law limits those decisions, and how roofing age affects insurance coverage long before any failure occurs.

In this article, we explain how these factors work together to help homeowners avoid sudden coverage issues and respond appropriately when insurers begin asking questions.

Why Roof Age Drives Insurance Decisions in Florida

Florida produces a unique insurance environment. Wind, humidity, salt air, and intense ultraviolet exposure accelerate the deterioration of roofing materials. Industry data consistently shows that roof-related losses are a large share of residential property claims across the state.

Insurance companies price policies based on probability, not appearance. A roof nearing the end of its expected service life increases the chance that wind-driven rain or minor uplift will cause interior damage. Once water enters a structure, the severity of the claim rises quickly.

That connection explains underwriting behavior. Insurers focus on roofs because roof failure often converts a manageable exterior repair into a full property insurance loss that involves drywall, flooring, electrical systems, and personal property.

The older the roof becomes, the harder it is for insurance companies to separate storm damage from long-term deterioration. And that uncertainty, in turn, directly affects coverage decisions.

How Old Can a Roof Be for Insurance in Florida?

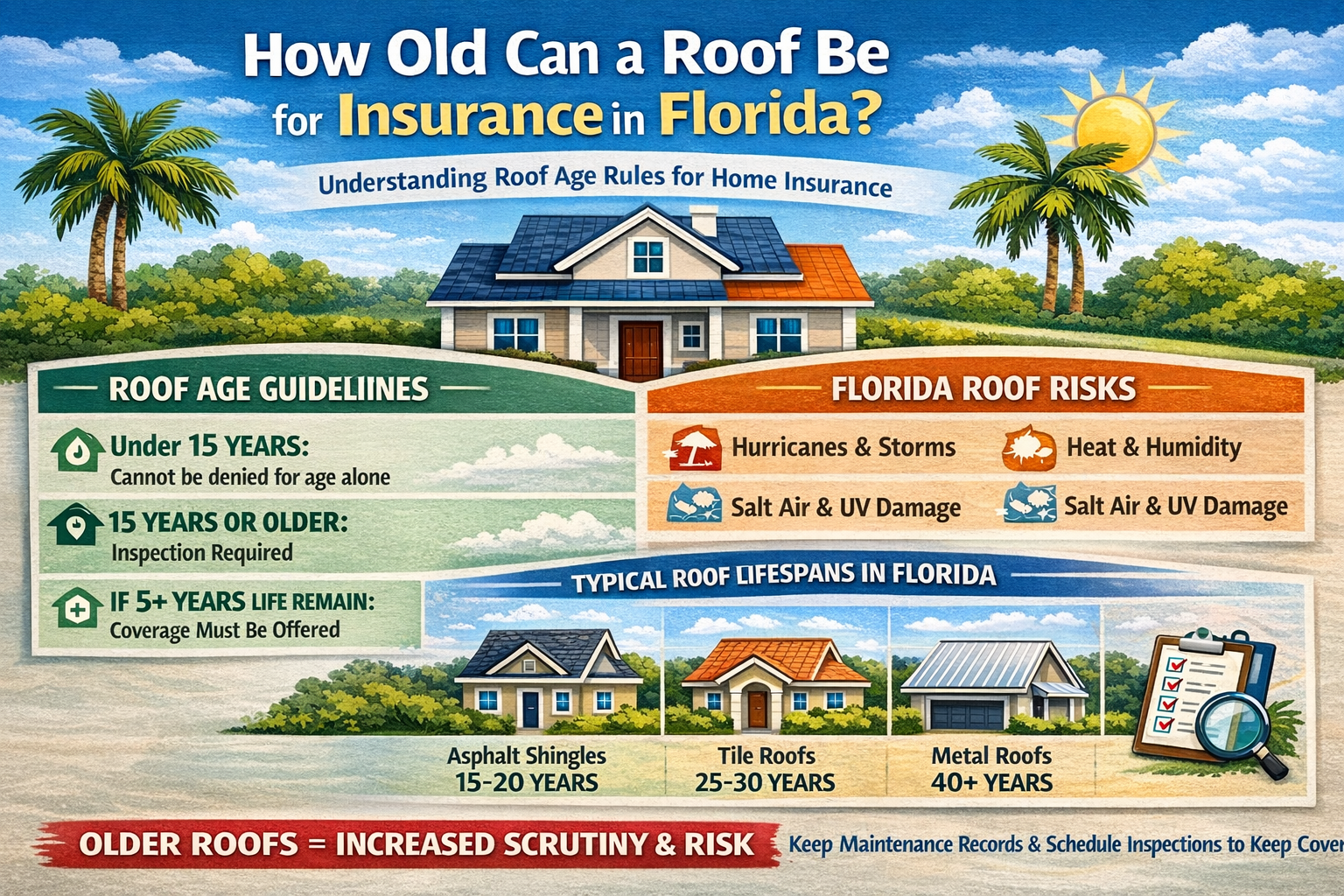

There is no single statewide cutoff age. Florida law instead regulates how insurers evaluate roofing.

Under Florida statute:

- A roof that is less than 15 years old cannot be rejected solely because of age.

- Once a roof reaches 15 years old, insurers may require an inspection.

- If an authorized inspector confirms at least five years of remaining useful life, insurers cannot refuse to issue or renew coverage based only on roof age.

This legal framework changed underwriting behavior across Florida, as age alone is no longer enough to deny homeowners private insurance. Condition must now be considered.

The rule exists because many Florida homeowners previously lost coverage even when their roofs remained functional.

The Real Meaning of the 15-Year Roof Rule in Florida

The so-called 15-year roof rule often creates confusion. The law does not require homeowners to get a new roof every fifteen years. Instead, it prevents automatic denial without evaluation.

Insurers may still review the roof’s age and condition, adjust premiums, or request documentation. The inspection requirement shifts the discussion from assumption to evidence.

In practical terms, the inspection becomes a risk clarification tool. A documented roof inspection reduces uncertainty for insurers. Less uncertainty often leads to the continued issuing or renewing of policies.

Roof Requirements for Homeowners Insurance in Florida

Florida homeowners’ insurance roof requirements combine statutory protections with underwriting analysis.

Insurance companies typically evaluate:

- Roofing materials and methods of installation

- Visible wear patterns

- Roof repair history

- Compliance with building code standards

- Wind resistance features

- Maintenance records

Each factor answers a single question: Does the roof still function as a reliable weather barrier?

If insurers believe water intrusion risk is rising, they may change policy terms even when coverage remains available.

Why Insurance Companies Scrutinize Older Roofs

Older roofs introduce a problem insurers call causation uncertainty.

After a storm, damage must be linked to a sudden event to qualify for insurance coverage. Aging roofs blur that distinction. Cracked shingles, worn underlayment, or fastener fatigue can appear similar to wind damage, which makes it harder to determine whether the loss resulted from a specific storm or long-term deterioration.

Because of this overlap, insurance companies often apply closer scrutiny to older roofs. Statistics from state regulatory discussions show roof claims account for a disproportionate share of litigation and claim disputes in Florida. The underwriting response is predictable: inspections, documentation requests, and valuation adjustments.

Many homeowners first encounter this scrutiny when a claim that appears straightforward turns into requests for additional inspections or detailed documentation. When causation becomes difficult to establish, insurers may question the scope of damage, limit repairs, or apply depreciation more aggressively. The issue is rarely the age of the roof alone, but the uncertainty surrounding how and when the damage occurred.

Typical Insurance Company Decision Process for Aging Roofs

Most insurance companies follow a similar progression when evaluating older roofs. What appears to homeowners as a sudden change is usually the result of a gradual underwriting process that develops over time.

- Internal data flags the roof based on age, prior inspections, or regional loss trends.

- Renewal review begins, often triggering requests for documentation or a roof inspection.

- Inspection results adjust risk scoring, helping insurers evaluate remaining useful life and overall condition.

- Coverage terms are modified, repriced, or continued depending on how clearly the risk can be assessed.

- Future claims receive closer causation review, particularly when damage could be attributed to either aging or a specific storm event.

Many Florida homeowners experience this progression as a sequence of renewal notices, inspection requests, and gradual policy adjustments rather than immediate cancellation. Insurance companies rarely terminate coverage outright. Instead, they shift financial exposure over time through valuation changes, updated deductibles, or revised policy terms.

Roof age alone does not determine coverage. What matters is how clearly insurers can evaluate risk. As roofs grow older, uncertainty increases, and insurance decisions often begin to change long before visible problems appear. When homeowners understand this pattern, renewal requests and inspections become easier to interpret, allowing preparation instead of reaction.

Will Insurance Cover a 20-Year-Old Roof?

Yes, insurance may still cover a 20-year-old roof. Coverage depends on material type, maintenance history, and inspection results.

Typical insurer expectations include:

- Asphalt shingles: about 15–20 years in Florida conditions

- Tile roofs: 25–30 years, depending on the underlayment condition

- Metal roofs: often 40 years or more with the right maintenance

A well-maintained metal roofing system may qualify long after a shingle roof reaches replacement discussions.

Coverage also depends on the cause. Insurance policies cover sudden damage such as wind or debris impact. Gradual deterioration remains excluded.

This distinction explains why two roofs of the same age can receive very different claim outcomes.

Florida Roofing Insurance Requirements and Building Code Changes

Florida roofing insurance requirements evolved after legislative reforms and building code updates that reduced claim disputes.

One major change involved the modification of the former 25% roof replacement rule. Homes that are built under newer building code standards may allow targeted repairs, not full roof replacements, when damage occurs.

Updated building code provisions strengthened fastening systems, underlayment installation, and wind resistance requirements. Insurers view code-compliant roofs as lower risk because they perform better during hurricanes.

That performance history influences underwriting decisions both in residential roofing and commercial roofing.

How Roof Age Changes Insurance Coverage Over Time

Home insurance coverage rarely disappears overnight. Instead, insurance companies adjust exposure gradually. These changes happen because insurers attempt to limit future payout exposure while still adhering to the insurance policy.

Common transitions include:

- Replacement cost value shifting toward actual cash value

- Higher deductibles applied to roof claims

- Inspection requirements before renewal

- Limited roof replacement benefits

- Increased premiums tied to risk scoring

Many Florida homeowners interpret these shifts as arbitrary. In reality, they reflect actuarial models reacting to expected loss patterns.

Florida Homeowners Insurance with Old Roofs: What Usually Happens

Many Florida homeowners encounter the same sequence:

- The roof is approaching its expected years of life

- Renewal notice requests documentation

- Premium increases or coverage changes appear

- Inspection becomes required

- Policy terms adjust depending on findings

Insurance companies rarely cancel immediately. What they do instead is shift financial responsibility gradually through valuation methods and underwriting restrictions.

Understanding this progression helps homeowners respond early rather than reacting under deadline pressure.

Why Material Type Changes the Outcome

Roofing materials influence risk differently. Insurance companies evaluate roofing materials because performance history directly affects claim frequency. Material choice, therefore, affects both eligibility and long-term premium stability.

- Asphalt shingles deteriorate faster under heat and humidity.

- Roofs of concrete tile often last longer structurally, but depend heavily on underlayment.

- Metal roofs resist wind uplift and fire risk, which sometimes results in insurance discounts.

Where PICC FLA’s Claim Review Work Becomes Relevant

Insurance policies rely heavily on interpretation. Scope of damage, depreciation calculations, and causation analysis determine how much coverage applies.

PICC FLA works with Florida property owners to review claims when settlement decisions do not align with observed damage or policy language. That review examines inspection findings, insurer estimates, and valuation methods used during adjustment.

In certain situations, additional benefits remain available because documentation or policy provisions were not fully considered during initial claim handling.

The process focuses on clarification first, correction second.

Why Independent Claim Review Matters

Insurance adjusters working for carriers evaluate claims within company guidelines and settlement frameworks. A roof public adjuster reviews the same loss from the policyholder’s perspective, focusing on full scope documentation and policy interpretation.

When roof age becomes part of a coverage discussion, small differences in how damage is categorized can significantly affect valuation. Independent review helps ensure that conclusions about age, condition, and causation reflect the full evidence available.

What Florida Homeowners Can Do Before Problems Start

Preventive action changes outcomes more than emergency reaction. These steps reduce uncertainty during underwriting and strengthen future claims if damage occurs.

- Maintain records of roof maintenance

- Schedule periodic roof inspection evaluations

- Keep proof of installation dates and permits

- Address minor repairs early

- Understand the valuation terms inside the insurance policy

Frequently Asked Questions

What are Florida homeowners’ insurance roof requirements?

Roofs must remain structurally sound, properly maintained, and capable of protecting the home from water intrusion. Inspections may be required once roofs reach fifteen years of age.

Can insurance companies refuse to issue coverage due to roof age?

Florida law prevents refusal solely based on age under certain conditions, especially when inspections confirm remaining useful life.

Will insurance replace an older roof after a storm?

Coverage applies when damage results from a covered event rather than normal aging.

Do metal roofs help with insurance approval?

Metal roofing often performs well in underwriting evaluations due to durability and wind resistance.

Final Takeaway

- The relationship between roof age and insurance in Florida is based on risk evaluation, not a fixed expiration date for a roof.

- Current Florida homeowners’ insurance roof requirements prevent insurers from denying coverage automatically, but insurance companies may still adjust policies as a roof becomes older and uncertainty increases.

- A roof can remain insurable when its age and condition, maintenance history, and a professional roof inspection demonstrate remaining useful life.

- Most problems arise when documentation is missing or when insurers cannot clearly separate storm damage from normal wear on older roofs.

- As roofs age, insurance coverage may change through inspections, pricing adjustments, or valuation methods rather than immediate cancellation.

- Understanding how insurance in Florida evaluates roofing risk helps homeowners prepare before renewal reviews or claim disputes occur.

- Maintaining records, scheduling inspections, and addressing roof maintenance early can help protect eligibility for homeowners’ insurance and reduce future complications.

- Knowing how roofing decisions influence underwriting allows many Florida homeowners to protect their insurance policy, avoid unexpected coverage limitations, and maintain long-term financial stability.