Property damage often provides insights regarding the gap between what a policyholder expects from insurance and what the policy actually covers. Most insurance policies appear sufficient until a claim is filed. At that point, hidden coverage gaps become visible when repair decisions are already underway, and options are limited.

In many claims, this gap is anything but minor. It can represent thousands in unrecovered repair costs, delays in settlement, or damage that is entirely outside coverage. What appears to be complete insurance coverage on paper may function very differently during the claim process.

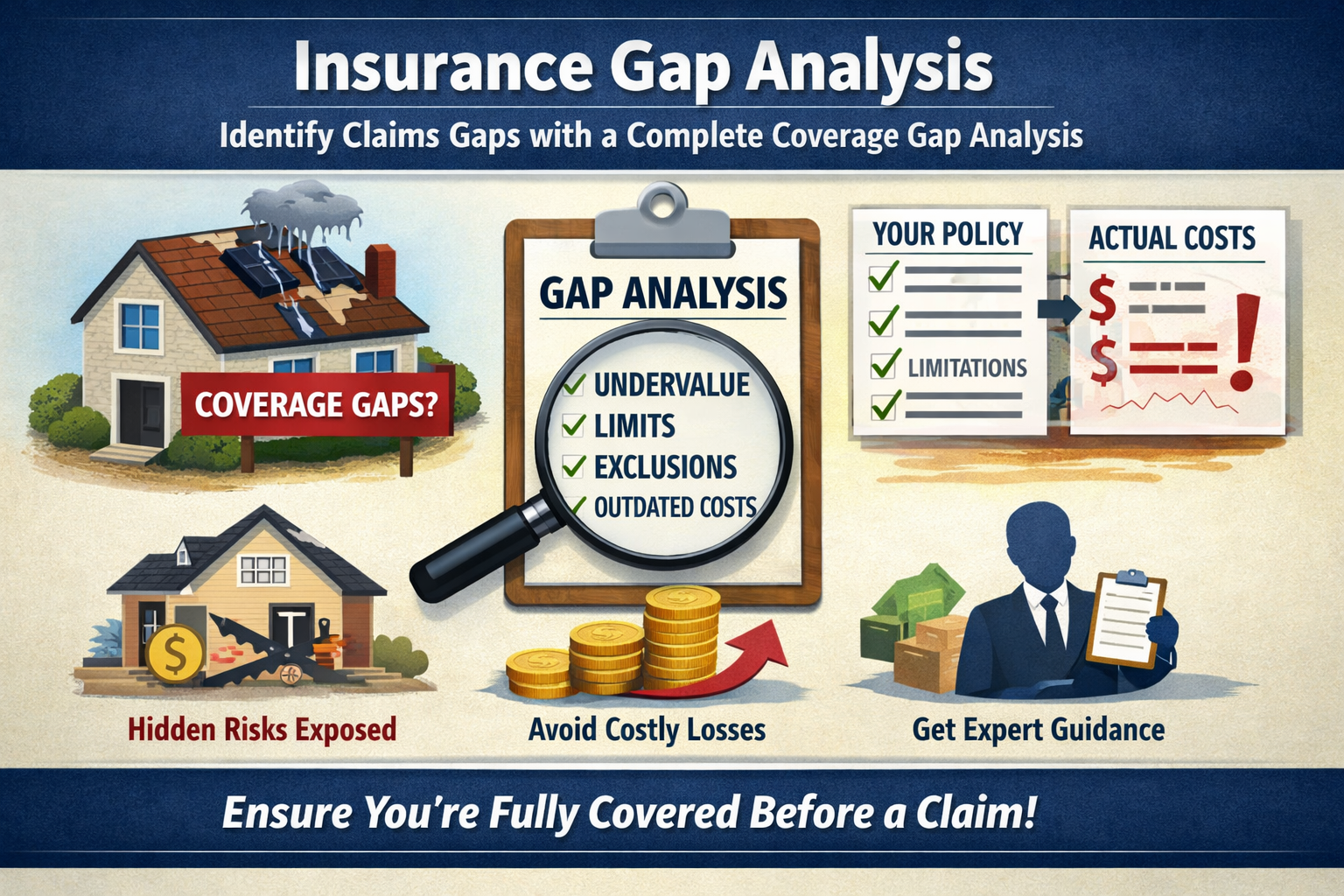

An insurance gap analysis evaluates how insurance coverage performs in real claim conditions. It identifies where a coverage gap exists, clarifies policy limitations, and determines if current coverage aligns with actual risks. Without this strategic analysis, policyholders often discover a gap only after a loss.

What Is an Insurance Gap Analysis?

An insurance gap analysis assesses whether current insurance policies provide adequate coverage for real exposure. This form of coverage gap analysis helps compare policy terms with the actual cost of restoring assets after damage.

The objective of a gap analysis is to identify discrepancies between insured limits, exclusions, and the true cost of repair or replacement. A coverage gap represents the difference between what the policy allows and what the loss requires.

This analysis reviews policy language, valuation methods, and claim conditions. It also evaluates whether current insurance reflects updated construction pricing, regulatory requirements, and evolving risks within the insurance industry. In practice, this strategy determines whether the policy performs as expected or falls short.

Why Most Insurance Policies Contain Coverage Gaps

Most insurance policies are not meant to eliminate all gaps. They operate within predefined limits, exclusions, and valuation methods that may not reflect actual risks.

One common issue involves outdated property value. When the insured amount does not reflect current restoration costs, a gap forms between available coverage and actual repair expenses. This difference becomes apparent only after contractor estimates exceed the insurer’s evaluation.

Exclusions create another type of gap. Certain causes of damage may not be covered at all, even though the policyholder assumed they were included. For example, water damage may be partially covered, while the underlying cause is excluded, leaving a portion of the loss outside coverage.

Changes in the insurance industry further contribute to these issues. As construction costs rise and regulatory requirements shift, older insurance policies may no longer provide adequate protection. Without a formal gap analysis, these hidden gaps remain undetected until a claim uncovers them.

How to Identify Claims Gaps Before and During a Claim

To identify claims gaps, the review requires evaluating how the insurance policy functions during an active claim, including how coverage is interpreted and applied.

A proper gap analysis examines limits, deductibles, exclusions, and valuation methods. It also compares contractor estimates with the insurer’s estimate to determine whether a gap exists in scope or pricing.

In many claims, this difference becomes clear when repair estimates exceed the insurer’s initial valuation. For example, a roof replacement may be priced based on current market conditions, whereas the insurer’s estimate is based on standardized pricing models. This creates a coverage gap between what is approved and what is required to complete the repair.

Data can help identify these inconsistencies. Estimating systems used in the insurance industry rely on uniform pricing structures, while construction costs vary. This disconnect often reveals a gap.

When these issues are identified before a loss, insurance coverage adjustments can be made to prevent underpayment.

Common Coverage Gaps That Lead to Financial Losses

Several recurring gaps appear in property claims and affect the success of the settlement.

A valuation gap happens when insured limits do not reflect current rebuilding costs. A limit-based gap develops when portions of a claim exceed sub-limits within the insurance policy. Exclusion-based gaps remove specific causes of damage from coverages, leading to out-of-pocket expenses.

Code upgrade gaps arise when building regulations require additional work that falls outside standard coverage. For businesses, interruption-related gaps affect income recovery when operational downtime is not fully covered.

In many claims, these gaps appear together. A property may be undervalued, partially excluded, and subject to limited restrictions at the same time. Each gap reduces the effectiveness of coverage, increasing exposure to potential risks and amplifying the total financial impact.

What Happens When Coverage Gaps Are Found in a Claim

When a coverage gap is identified during a claim, the financial impact is immediate. The insurance company evaluates the loss based on policy language, internal estimates, and documented damage.

In the event that portions of the loss fall outside coverage, they are excluded from payment. If the scope is incomplete or undervalued, the claim is reduced. In some cases, this results in partial settlements that do not reflect the full cost of repairs.

Without proper documentation, additional repairs may not be included in the claim. This creates a gap between the approved amount and the actual cost required to restore the property.

Multiple gaps can compound the issue. Each limitation reduces the final settlement, increasing the policyholder’s financial responsibility. The difference between expected coverage and actual payment becomes clear at this stage, often when repair work is already in progress.

The Technical Process Behind a Coverage Gap Analysis

A complete coverage gap analysis follows a structured analysis process. It begins with a detailed review of the insurance policy, including endorsements, exclusions, and coverage limits.

The next step evaluates the damage and compares it to the insurer’s scope. This phase of the gap analysis identifies discrepancies in pricing, scope, and interpretation of coverage.

From a risk management perspective, this analysis connects damage scenarios with policy performance. The gap analysis can reveal where the policy fails to respond as expected and where adjustments are required.

This process transforms complex policy language into a practical evaluation of claim performance, so policyholders understand how insurance coverage works in real conditions.

Why Handling Gap Analysis Without Expertise Is Risky

Interpreting an insurance policy requires technical expertise. Without it, identifying a gap and understanding its impact on coverage becomes difficult.

Insurance companies rely on internal systems, standardized pricing, and claim guidelines. Policyholders rely on their understanding of the property. This difference creates a situation where gaps in scope, pricing, or policy interpretation may go unchallenged.

For example, if a contractor identifies additional damage after repairs begin, but that damage was not included in the original estimate, it may not be added to the claim without proper documentation. This leaves a portion of the repair outside coverage, even though it is directly related to the loss.

Without professional review, these discrepancies remain unresolved, increasing the likelihood of reduced coverage.

How a Public Adjuster Identifies and Closes Coverage Gaps

A public adjuster performs a detailed gap analysis to evaluate how the insurance policy applies to the loss. This includes reviewing documentation, inspecting the property, and comparing estimates.

The goal is to identify where the insurer’s evaluation differs from actual repair requirements. Each identified gap is supported with documentation, pricing analysis, and policy interpretation.

This proactive approach produces specialized solutions that address valuation differences, scope omissions, and policy limitations. For clients, the result is a clear, documented position that supports a more accurate claim outcome.

Rather than relying on initial estimates, this analysis guarantees that coverage reflects the full scope of the damage.

When You Should Perform an Insurance Gap Analysis

A gap analysis should be performed before a loss and after any claim so that insurance policies reflect current risks and property conditions.

For individuals and businesses, changes in exposure create new gaps over time. When reviewing current insurance policies, coverage is better aligned with those changes.

In the real estate context, rising construction costs and updated regulations frequently create a gap between insured value and rebuilding cost. Periodic analysis helps maintain accurate coverage and reduce risk.

Conclusion: From Coverage Gaps to Complete Protection

A structured insurance gap analysis provides the understanding needed to evaluate how insurance coverage performs under real conditions. Identifying each gap allows policyholders to reduce exposure, avoid unexpected outcomes during a claim, and make informed decisions.

A comprehensive gap analysis connects policy terms, valuation, and claim performance into a clear framework. In this context, gap analysis can prevent significant financial loss as it identifies limitations before they affect the outcome of a claim.

Professional Coverage Gap Analysis by PICC FLA

PICC FLA provides thorough gap analysis services to evaluate how insurance responds to property damage. We review insurance policies, assess damage, and identify every coverage gap that may affect your claim.

Through a structured analysis, PICC FLA develops accurate documentation, strengthens claim presentation, and improves settlement outcomes.

If there is uncertainty about how your insurance policy will perform, a professional review can uncover hidden gaps before they affect your claim. Early identification lays the foundation for better decisions, stronger documentation, and satisfying results.

Contact us today!

Frequently Asked Questions About Insurance Gap Analysis

What is an insurance gap analysis, and why is it important?

An insurance gap analysis evaluates your insurance coverage and whether it aligns with your actual exposure. It is important because hidden gaps in insurance policies often reduce claim payments and increase out-of-pocket costs.

How can I identify claim gaps in my insurance policy

To identify claim gaps, you should review policy limits, exclusions, and valuation methods. These must be compared against actual repair requirements to reveal where coverage may fall short during a claim.

What are the most common coverage gaps in insurance policies?

Common gaps include undervalued property limits, excluded causes of loss, and restrictions. These issues can reduce the effectiveness of coverage when a claim is filed.

Should individuals and businesses perform a coverage gap analysis?

Both individuals and businesses face different risks, and each requires a tailored review to be sure insurance policies provide appropriate coverage.