Insurance appraisal can be a valuable solution when you believe your property damage claim has been undervalued. Whether you are dealing with hurricane damage, water intrusion, fire loss, roof damage, or another covered event, understanding the appraisal process can help you make informed decisions about your claim. This guide explains how insurance appraisal works, when it may be appropriate, and how experienced professionals can help you pursue a fair settlement while avoiding unnecessary delays and costly litigation.

At PICC FLA, we assist homeowners and business owners throughout the insurance appraisal process, providing free property inspections, complimentary policy reviews, and no recovery, no fee representation to help clients seek the compensation they may be entitled to receive.

Call Us Today For A FREE Claim Analysis

What Is a Home Insurance Appraisal?

A home insurance appraisal is a dispute resolution procedure used when the insured and the insurance company disagree regarding the financial value of a covered insurance claim.

These disputes commonly involve repair pricing, replacement cost value, actual cash value, or the overall scope of property damage. The insurance appraisal process does not generally define whether coverage exists under the policy itself. What it does, instead, is determine the appropriate compensation associated with the loss.

Most property insurance policies contain an insurance appraisal clause, sometimes referred to as an appraisal clause insurance provision. This section outlines the process in which either party may request an appraisal when there is a disagreement that involves the amount payable under the claim.

Compared to a real estate appraisal, an insurance appraisal is not intended to determine market value. The process practically resolves insurance claim appraisal disputes that include property damage assessments and repair estimates.

The insurance appraisal process is frequently used after hurricanes, water intrusion events, plumbing failures, fire losses, smoke damage, roof leaks, broken pipes, AC leaks, and commercial property damage claims. In many of these cases, the insurer acknowledges the claim while disputing the amount necessary to complete the required repairs and remediation work.

For policyholders who deal with underpaid claims, the appraisal process may work as an effective alternative to litigation.

Key Takeaways

- The home insurance appraisal process helps resolve disputes over underpaid property insurance claims.

- Insurance appraisal usually addresses repair costs, damage scope, and claim valuation, not coverage disputes.

- Either the policyholder or the insurance company can typically request an appraisal under the insurance appraisal clause.

- The process is commonly used after hurricanes, water damage, fire losses, roof leaks, and plumbing failures.

- Insurance appraisals may resolve disputes faster and at a lower cost than litigation.

- At PICC FLA, we provide free inspections, free policy review, and no recovery, no fee representation.

How the Insurance Appraisal Process Helps Resolve Claim Disputes

After a hurricane, plumbing leak, fire, or significant water intrusion, most property owners expect their private insurance company to issue a settlement sufficient to complete the necessary repairs. In practice, many homeowners and business owners discover that the insurer’s estimate does not reflect the actual extent of damage or the cost of reconstruction.

This is where the home insurance appraisal process is key. In many situations, the insurance company acknowledges that the loss is covered while disputing repair pricing, limiting the damage assessment, or omitting related deterioration identified after the initial inspection. Policyholders then evaluate whether to accept the settlement, pursue litigation, or formally challenge the insurer’s valuation.

The insurance appraisal process provides an alternative mechanism for resolving these disputes.

Rather than immediately entering prolonged litigation, with appraisal, both parties can evaluate the claim through independent appraisers and, when necessary, a neutral umpire. For Florida property owners, the process is commonly used after hurricanes, water damage, fire losses, roof leaks, broken pipes, plumbing failures, and other property-related losses that involve disputed repair valuations.

When Should You Start the Insurance Appraisal Process?

The homeowners’ insurance appraisal process commonly begins after the insurance company has issued payment, but the amount offered does not adequately cover the documented repairs.

An insurer may approve the claim while continuing to dispute the repair scope, labor pricing, material costs, code upgrade requirements, replacement recommendations, or the extent of concealed damage affecting walls, flooring systems, roofing assemblies, cabinetry, or structural components.

Water damage claims are a common example. Insurance companies may account for visible damage yet exclude trapped moisture, compromised insulation, warped subflooring, microbial contamination, or secondary deterioration identified later during remediation.

Following hurricanes, insurers also often underestimate roofing systems, structural movement, interior water intrusion, and additional damage associated with prolonged exposure.

With the insurance appraisal process, policyholders can formally challenge these valuation disputes without immediately initiating litigation.

However, timing remains important. Insurance policies contain different deadlines, appraisal conditions, and notice requirements. In some situations, appraisal rights may later become disputed if legal proceedings have already advanced significantly.

For that reason, policyholders should review their policy carefully before making major claim decisions.

At PICC FLA, we perform on-site evaluations, review the applicable policy language, and determine whether appraisal for insurance purposes is the appropriate strategy for the claim.

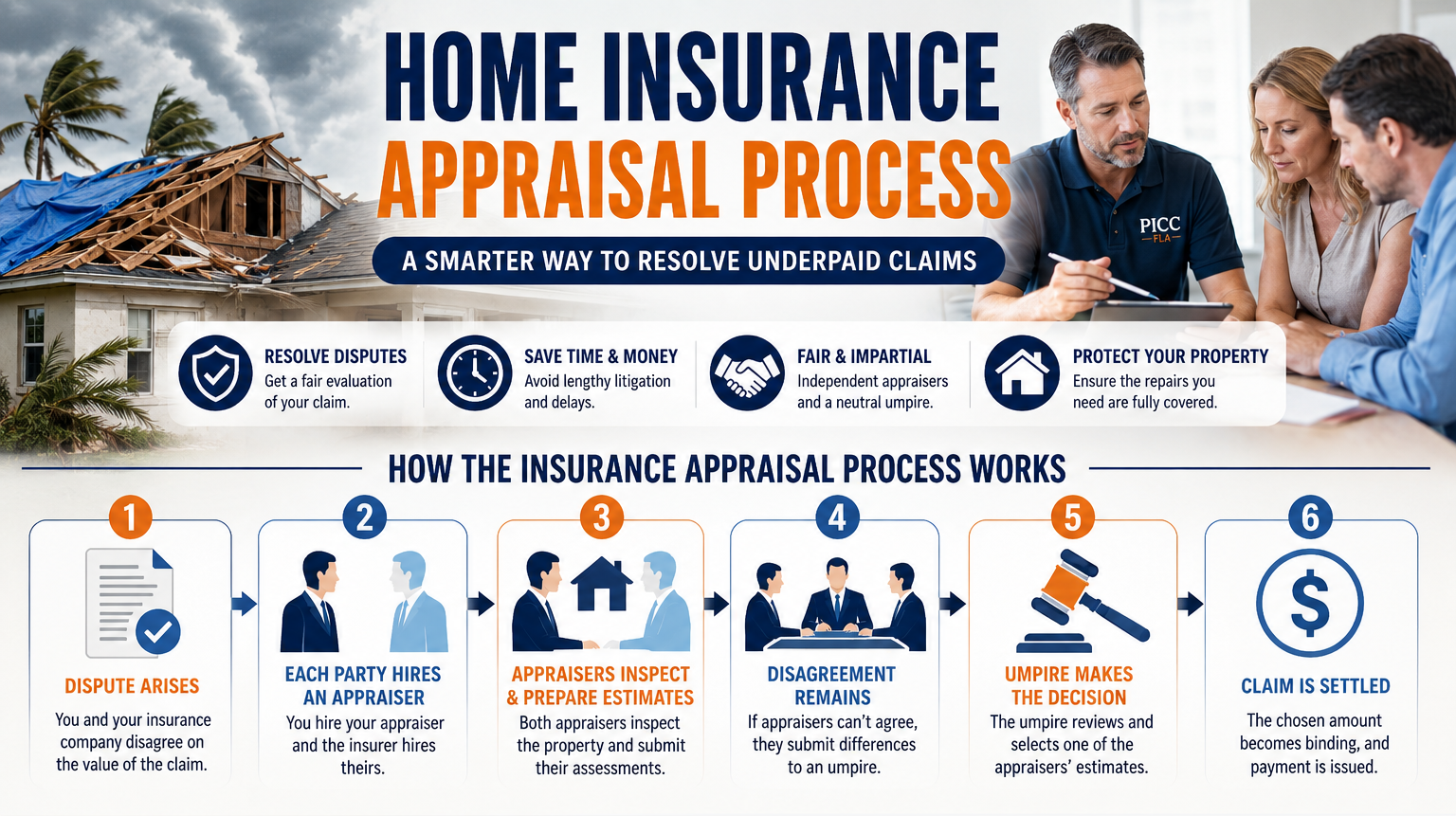

How Does the Insurance Appraisal Process Work in Florida?

Understanding how the appraisal process works can help property owners avoid procedural mistakes during a disputed insurance claim.

The insurance appraisal process that Florida policyholders encounter generally begins when either the insured or the insurance company submits a written demand for appraisal under the insurance policy.

Once an appraisal is invoked, each side selects its own appraiser. The policyholder appoints an independent appraiser, while the insurer appoints its own insurance claim appraiser. The appraisers then evaluate the property, review repair estimates, analyze the damage, and attempt to reach an agreement regarding the claim valuation.

At PICC FLA, we conduct in-person damage assessments because significant property damage is frequently overlooked during desk reviews or photo-only evaluations. Moisture intrusion, structural deterioration, smoke contamination, roofing failures, and secondary water damage often extend beyond what appears in the insurer’s original estimate.

If the appraisers cannot agree on the value of the claim, they select an umpire. The umpire functions as a neutral third party responsible for reviewing disputed items and assisting with the final valuation determination.

If the appraisers cannot mutually agree upon an umpire, either party may petition the court to appoint one.

Once the umpire becomes involved, the appraisal panel reviews the disputed valuation items. Any decision signed by two members of the panel becomes binding. This means either both appraisers agree, or one appraiser and the umpire agree regarding the final award.

The appraisal process may resolve disputes about replacement cost value, actual cash value, repair pricing, scope disagreements, and other valuation issues associated with property insurance claims.

Insurance Appraisal vs Lawsuit: What’s the Difference?

Many property owners assume litigation is the only method to challenge an underpaid insurance settlement. In reality, insurance appraisals may often resolve valuation disputes more efficiently and at a lower overall cost.

The appraisal process is generally narrower in scope and less adversarial than litigation because it focuses specifically on the financial disagreement surrounding the claim and not the broader legal disputes regarding coverage determinations or bad-faith allegations.

Attorneys primarily focus on legal procedure, litigation strategy, and contract interpretation. Public adjusters and insurance claims appraiser professionals focus on evaluating property damage, assessing repair costs, documenting overlooked conditions, and determining what is necessary to complete the reconstruction work.

That distinction matters more than you think.

At PICC FLA, we do not rely solely on remote documentation reviews. We evaluate the property firsthand, identify underestimated conditions, assess repair requirements, and document issues insurers often miss during initial inspections.

Cost considerations also impact many policyholders’ decisions. Attorneys commonly charge contingency fees approaching 40%, while public adjusters generally operate at substantially lower percentages. PICC FLA works on a no recovery, no fee basis and does not require upfront costs.

That said, appraisal process insurance disputes are not appropriate for every situation. Insurance appraisal generally addresses valuation disagreements involving repair costs, replacement value, actual cash value, or damage scope. It does not typically determine whether the claim itself is covered under the policy.

Why Policyholders Hire a Public Adjuster for Insurance Appraisal

Insurance companies rely on experienced adjusters, engineers, consultants, and internal estimating teams whose responsibility is to protect the insurer’s financial position. Policyholders should have representation that can protect their interests.

That is one reason many homeowners and business owners retain a public adjuster during the insurance appraisal process.

A qualified appraiser may identify conditions that were underestimated, excluded, or omitted entirely from the insurance company’s estimate.

At PICC FLA, we perform property-level inspections because no estimate should rely entirely on photographs or software-generated pricing models. Our expertise is based on firsthand damage analysis and practical understanding of the work that’s required to return the property to a safe and functional condition.

We also assist policyholders throughout South Florida with appraisal clause review, policy interpretation, damage documentation, repair valuation analysis, and navigation of the broader insurance appraisal process.

Every claim presents different damage conditions, policy language, and reconstruction requirements. For that reason, each appraisal strategy must be adjusted to the specific loss.

Common Property Damage Claims That Go to Appraisal

Insurance appraisals are commonly used when policyholders and insurance companies disagree about the appropriate cost to repair damaged property.

- Hurricane claims remain among the most common appraisal-related disputes in Florida because insurers frequently underestimate roofing systems, structural conditions, interior water intrusion, and secondary moisture damage after major storms.

- Water damage claims also routinely proceed to appraisal. Broken pipes, plumbing leaks, water heater failures, drain backups, and AC leaks may create concealed damage that affects walls, flooring systems, insulation, cabinetry, and structural materials that insurers fail to adequately include in their estimates.

- Fire and smoke claims often involve disagreements regarding demolition requirements, odor remediation, electrical damage, smoke contamination, and reconstruction expenses.

- Commercial property claims may become even more complex because they frequently involve larger repair scopes, specialized materials, operational interruptions, and higher-value structural losses.

In many of these situations, the disagreement centers on the appropriate cost necessary to complete repairs and remediation work associated with the loss.

That is precisely where the insurance appraisal process can help. Call us today for more information.

Get Help With the Insurance Appraisal Process in Florida

If your insurance company acknowledged the claim but issued a settlement that does not fully address the documented damage, additional options may still be available.

At PICC FLA, we help homeowners and business owners challenge underpaid property insurance claims through the insurance appraisal process. Our team conducts direct property evaluations, documents the damage thoroughly, and advocates for the compensation necessary to complete the required repairs.

We handle hurricane claims, water damage, fire losses, plumbing failures, roof damage, broken pipes, drain backups, AC leaks, and other property-related insurance disputes throughout South Florida.

We also provide free inspections, free policy review, no upfront fees, and no recovery, no fee representation.

Before accepting an undervalued settlement, review the policy carefully and have the property evaluated by professionals working on your behalf rather than the insurance company’s.