A homeowner’s insurance claim denied notice can be frustrating, especially when your property is already damaged, and repair costs are rising. Many Florida homeowners receive a denied home insurance claim after hurricanes, roof leaks, broken pipes, AC overflows, fire damage, or water intrusion, often because the insurance company disputes the cause of loss, limits the scope of repairs, or overlooks hidden damage during the inspection.

The good news is that a denial does not always mean your claim is over. In many cases, homeowners discover that important damage was missed, repair costs were underestimated, or policy provisions were interpreted too narrowly. If you’re wondering what to do if homeowners’ insurance denies a claim or how to appeal a denied home insurance claim, understanding the true extent of the damage is often the first step toward a successful outcome.

At PICC FLA, we work with homeowners facing denied property insurance claims every day. Our team performs detailed property inspections, reviews policy language, evaluates repair requirements, and identifies damage that may have been overlooked during the original investigation. Whether you’re trying to understand how to fight a denied homeowners insurance claim or simply want a professional second opinion, we help you determine the strongest path forward.

Before accepting the insurance company’s decision, take the time to understand your options. The information below explains the most common reasons claims are denied, the steps you can take to protect your rights, and how professional claim representation may help recover the compensation needed to restore your property properly.

Key Takeaways

- A homeowner’s insurance claim denied decision does not always mean the damage is uncovered or correctly evaluated.

- Roof, water, plumbing, and hurricane claims are frequently disputed because underlying damage is often missed during inspections.

- Successful appeals usually depend on inspections, documentation, repair analysis, and technical evidence.

- Public adjusters represent policyholders, not insurance companies, and focus on identifying damage and documenting the full repair scope.

- PICC FLA offers free inspections, free policy reviews, no upfront fees, and a no recovery, no fee structure.

Signs Your Insurance Company May Have Wrongfully Denied Your Claim

A denial deserves closer review when the insurer’s explanation does not match the actual condition of the property.

One of the clearest warning signs is a limited inspection. Water intrusion claims often involve damage hidden behind cabinets, inside drywall cavities, beneath flooring systems, or within insulation materials. Roof claims may involve compromised flashing, lifted underlayment, punctured membranes, or storm-created openings that are not visible from ground-level photographs.

Another concern involves broad maintenance allegations unsupported by testing or invasive inspection. Insurers frequently deny claims by citing wear and tear, deterioration, seepage, or pre-existing conditions without fully documenting how they reached those conclusions.

Some denials acknowledge limited damage while excluding major portions of the restoration process. Flooring replacement may be omitted. Moisture remediation may be excluded. Matching materials, cabinetry removal, roof decking repairs, or code-required upgrades may never appear in the insurer’s estimate.

That does not necessarily mean the damage is uncovered. In many cases, it reflects a dispute over the actual repairs required to restore the property.

What to Do if Home Insurance Denies Your Claim

If you received a denied homeowners insurance claim, do not assume the insurer’s decision is automatically correct. Many insurance claim denials stem from disputed causation, incomplete inspections, maintenance allegations, or underlying damage that was never fully documented.

Start by reviewing the denial letter carefully. The insurer should explain all reasons why the claim was denied and identify the policy language supporting the decision. If the explanation is vague, request additional information before deciding whether to file an appeal or dispute the findings.

Then compare the denial against the actual property conditions. Water intrusion from an AC overflow, broken pipe, or roof leak may continue spreading behind walls, beneath flooring systems, or inside insulation long after visible symptoms first appear. Hurricane claims may also involve roof or structural damage overlooked during the original inspection.

This is why many homeowners researching what to do when homeowners’ insurance denies a claim pursue independent evaluations. Contractors, engineers, roofers, mitigation specialists, and public adjusters often uncover trapped water, incomplete repair scope, or restoration requirements missing from the insurer’s estimate.

Once a claim is denied, the dispute usually shifts toward proving the true extent of the damage through inspections, documentation, repair analysis, and technical evidence.

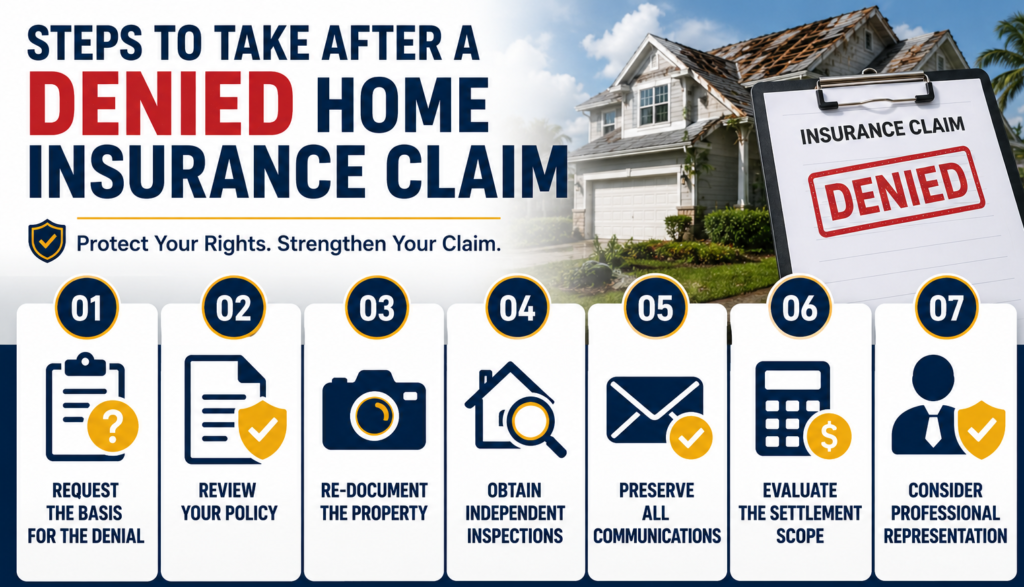

Steps to Take After a Denied Home Insurance Claim

Step 1: Request the complete basis for the denial

The insurer should clearly explain why the claim was denied and identify the policy provisions supporting the decision. Broad references to wear and tear or to excluded water damage are not enough if the carrier cannot connect those conclusions directly to the property’s condition.

Step 2: Review the policy carefully

Many disputes involving a home insurance claim denial arise from disagreements over exclusions, endorsements, water damage provisions, matching requirements, or reporting obligations buried in the policy language.

Reviewing home insurance policies carefully is important because insurance policies contain conditions that directly affect whether a loss is covered. Properly understanding your policy may reveal that the denial language was applied too broadly.

Step 3: Re-document the property

Once a claim is denied, the dispute usually centers on proving scope, causation, and repair necessity. Photograph damaged framing, warped materials, cracked roofing components, deteriorated subflooring, smoke contamination, or demolition findings not fully documented during the original inspection.

Step 4: Obtain independent inspections

Second inspections routinely uncover trapped water beneath flooring systems, roof penetration points, saturated insulation, deteriorated decking, or structural damage never documented during the original inspection.

Independent inspections also help build stronger evidence when a claim denial involves disputed causation or incomplete repair findings.

Step 5: Preserve every communication and timeline

Denied claims often become disputes over what was reported, when it was reported, and what information the insurer reviewed before issuing its decision. Save emails, invoices, estimates, inspection summaries, photographs, mitigation records, and written communications.

This documentation becomes important if the policyholder later decides to file a complaint with the state insurance department or pursue additional dispute resolution options.

Step 6: Evaluate whether the settlement scope is incomplete

Some insurers partially pay claims while excluding critical repairs. These under-scoped estimates can function as practical denials because the settlement is insufficient to restore the property properly.

Step 7: Consider professional representation

Homeowners researching how to fight a denied homeowners insurance claim often discover the dispute has become highly technical. Structural drying, roofing systems, demolition scope, code compliance, and repair methodology all influence claim valuation. Public adjusters evaluate those issues directly through property inspection and detailed estimate preparation.

How to Appeal a Denied Insurance Claim

Effective appeals challenge the carrier’s conclusions with evidence capable of changing how the claim is evaluated.

Strong appeals often include revised repair estimates, contractor evaluations, engineering analysis, plumbing reports, roofing inspections, demolition photographs and videos, or mitigation records showing the original inspection failed to capture the full extent of damage.

An effective appeal addresses each disputed issue directly and supports every disagreement with evidence tied to the actual loss conditions.

What Happens if Your Insurance Appeal is Denied?

When an appeal fails, homeowners often believe the claim is permanently closed. However, denied claims can sometimes be reopened if additional damage is discovered during demolition, reconstruction, or supplemental inspection.

A denied appeal can also expose broader claim handling concerns. Some insurers rely heavily on limited testing, generalized engineering summaries, or narrow visual inspections that fail to evaluate concealed damage thoroughly. Others repeatedly request documentation while delaying claim resolution or shifting explanations regarding coverage.

Some policyholders eventually pursue mediation, regulatory review through the department of insurance, or legal action if the insurance company will not reevaluate the loss despite substantial supporting evidence.

For many homeowners, the issue evolves beyond simply asking “insurance claim denied, what to do” and becomes a question of whether the insurer conducted a complete and accurate investigation before refusing payment.

Can a denied claim be reopened?

Yes. A denied claim may sometimes be reopened if new evidence, secondary damage, supplemental inspections, or additional repair findings emerge after the original evaluation.

This often happens when demolition reveals trapped water, structural deterioration, roof system failures, or secondary damage that was not visible during the insurer’s initial inspection.

Denied Roof, Water, and Hurricane Insurance Claims

Roof, water, and hurricane claims generate some of the most aggressive insurance disputes in Florida because these losses often involve concealed damage, complex causation analysis, and expensive restoration requirements.

- Roof claims are commonly denied based on allegations involving aging materials, installation defects, cosmetic damage, or prior deterioration. However, lifted shingles, punctured membranes, displaced flashing, compromised underlayment, and storm-created openings may still allow significant water intrusion into the structure.

- Water damage claims involving broken pipes, slab leaks, drain backups, AC overflows, and water heater failures are heavily contested because coverage often depends on whether the damage resulted from a sudden event or long-term leakage.

- Hurricane claims create additional complexity because insurers may separate wind damage, flood damage, and pre-existing conditions into different categories during evaluation. Interior water intrusion, roof uplift, saturated insulation, damaged windows, compromised framing, and structural moisture often require invasive inspection before the true repair requirements become clear.

How a Public Adjuster Can Help with a Denied Property Insurance Claim

A public adjuster represents the policyholder. In a homeowners’ claim denied situation, the public adjuster investigates the property directly, evaluates the restoration scope, documents damage, reviews policy language, and negotiates based on the actual condition of the structure.

Compared to an insurance adjuster working for the carrier, a public insurance adjuster evaluates the loss from the policyholder’s perspective and prepares documentation designed to support your claim fully.

Public adjusters inspect roofing systems, flooring assemblies, structural cavities, smoke damage patterns, and demolition findings to determine whether the insurer’s estimate accurately reflects the loss.

In many denied claims, the dispute involves whether the insurer excluded secondary water intrusion, structural damage, remediation costs, matching materials, code-required upgrades, demolition costs, or repairs necessary to complete restoration properly.

Public adjusters also organize supporting evidence from contractors, mitigation companies, engineers, plumbers, roofers, and restoration specialists whose findings may directly contradict the insurer’s conclusions.

Because public adjusters generally work on contingency, policyholders typically do not pay upfront fees. Compensation is based on a percentage of the settlement recovered from the insurer.

Why Work with PICC FLA?

PICC FLA represents homeowners and business owners throughout South Florida with claims involving hurricanes, roof leaks, plumbing failures, broken pipes, AC overflows, fire damage, smoke contamination, water intrusion, and other residential or commercial property losses.

The company’s approach centers on direct property investigation. PICC FLA inspects the structure itself to identify deterioration, incomplete repair scope, under-scoped estimates, and restoration requirements that may not have been fully documented during the original claim review.

This becomes especially important in denied and underpaid claims, where secondary damage is often overlooked. Damage beneath flooring systems, compromised roof decking, saturated insulation, smoke contamination inside HVAC systems, and structural deterioration inside wall cavities may substantially increase the true cost of restoration.

PICC FLA documents those conditions through photographs, estimates, inspection findings, contractor evaluations, and detailed claim preparation designed to support a more accurate presentation of the loss.

While attorneys often become involved later in the dispute process, public adjusters focus directly on identifying damage, evaluating repair requirements, and documenting restoration needs before repair costs escalate further.

The company offers free inspections, free policy reviews, no upfront fees, and a no recovery, no fee structure for qualifying claims.